A new analysis released by the National Federation of Independent Business outlines the projected economic impact of the now‑permanent 20 percent Small Business Tax Deduction, a federal change NFIB says prevents a major tax increase on most Wisconsin small businesses.

The deduction, known as Section 199A, allows eligible pass‑through businesses to deduct up to 20 percent of qualified business income. It was scheduled to expire at the end of 2025. Congress approved legislation extending it, and President Trump signed the measure on July 4, 2025.

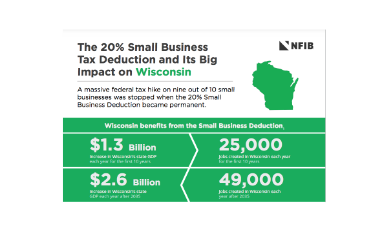

NFIB’s Wisconsin impact sheet estimates the permanent extension will generate about 25,000 new jobs per year in the state over the next decade. The report also projects an annual increase of roughly 1.3 billion dollars in Wisconsin’s GDP during that period. After 2035, the analysis estimates the state could see 49,000 new jobs per year and a 2.6 billion dollar annual GDP increase.

Luke Bacher, NFIB’s Wisconsin state director, said the permanence of the deduction gives small employers the certainty they need to plan for hiring and investment.

“By making the 20% Small Business Tax Deduction permanent, Congress has provided the relief needed to help Wisconsin small businesses invest in their employees and operations,” Bacher said. “This means more competitive wages and a more resilient local economy for years to come.”

NFIB cites research from EY that warns nine out of ten small businesses would have faced a combined top tax rate of 47.25 percent without the deduction. The organization argues that avoiding that increase frees up capital for payroll, equipment, and expansion.

Additional federal tax changes

The report highlights several other federal tax provisions that were made permanent alongside the deduction:

- Section 179 expensing: The cap was doubled from 1.25 million dollars to 2.5 million dollars and indexed to rise annually. The change allows small businesses to deduct the full purchase price of qualifying equipment in the year it is acquired.

- Bonus depreciation: The first‑year deduction under Section 168(k) was restored to 100 percent for eligible assets placed in service after January 2025. Before the change, businesses had to depreciate property over longer schedules.

- Estate tax exemption: The exemption was permanently increased to 15 million dollars for individuals and 30 million dollars for joint filers, with inflation adjustments. NFIB says the higher threshold helps family‑owned businesses avoid selling assets to cover federal estate tax liabilities.

NFIB argues that the combination of these provisions gives small employers more flexibility to invest in equipment, maintain property, and plan for generational transitions.

Wisconsin’s small‑business landscape

Wisconsin is home to 497,370 small businesses, according to the U.S. Small Business Administration. Those firms employ about 1.2 million workers statewide, making small employers a central part of the state’s workforce and economic base.

NFIB says the permanent tax changes will help those businesses compete with larger corporations by allowing them to retain more of their earnings. The organization also points to projected national impacts, including an estimated 75 billion dollar annual increase in U.S. GDP over the next decade and 1.2 million new jobs per year nationwide.

Why it matters for Wisconsin

The report arrives as Wisconsin continues to navigate workforce shortages, rising operating costs, and uneven economic growth across regions. NFIB argues that long‑term tax certainty is a key factor in whether small employers expand, hire, or invest in new equipment.

The organization says the permanence of the deduction and related provisions gives small businesses a clearer planning horizon, which it believes will translate into job creation and higher wages.

Wisconsin’s state‑specific report and the national analysis are available on NFIB’s website.

{kind=link}